Adjusted Trial Balance Format Preparation Example Explanation

Textbook content produced by OpenStax is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License . This book may not be used in the training of large language models or otherwise be ingested into large language models or generative AI offerings without OpenStax’s permission.

Format

This means we must add a credit of $4,665 to the balance sheet column. Once we add the $4,665 to the credit side of the balance sheet column, the two columns equal xero expenses on the app store $30,140. In the Printing Plus case, the credit side is the higher figure at $10,240. This means revenues exceed expenses, thus giving the company a net income.

4 Use the Ledger Balances to Prepare an Adjusted Trial Balance

When one of these statements is inaccurate,the financial implications are great. Financial statements give a glimpse into the operations of a company, and investors, lenders, owners, and others rely on the accuracy of this information when making future investing, lending, and growth decisions. When one of these statements is inaccurate, the financial implications are great. The adjusting entries for the first 11 months of the year 2015 have already been made. Review the annual report of Stora Enso which is aninternational company that utilizes the illustrated format inpresenting its Balance Sheet, also called the Statement ofFinancial Position. Discover the best business bank accounts for sole proprietors in 2025, comparing top banks to help you find the perfect fit for your needs.

Accounting

- Both US-based companies and those headquartered in other countries produce the same primary financial statements—Income Statement, Balance Sheet, and Statement of Cash Flows.

- Looking at the income statement columns, we see that all revenue and expense accounts are listed in either the debit or credit column.

- It’s one of the first lines of defense against accounting errors and a pivotal report within double-entry bookkeeping.

- To get the $10,100 credit balance in the adjusted trial balance column requires adding together both credits in the trial balance and adjustment columns (9,500 + 600).

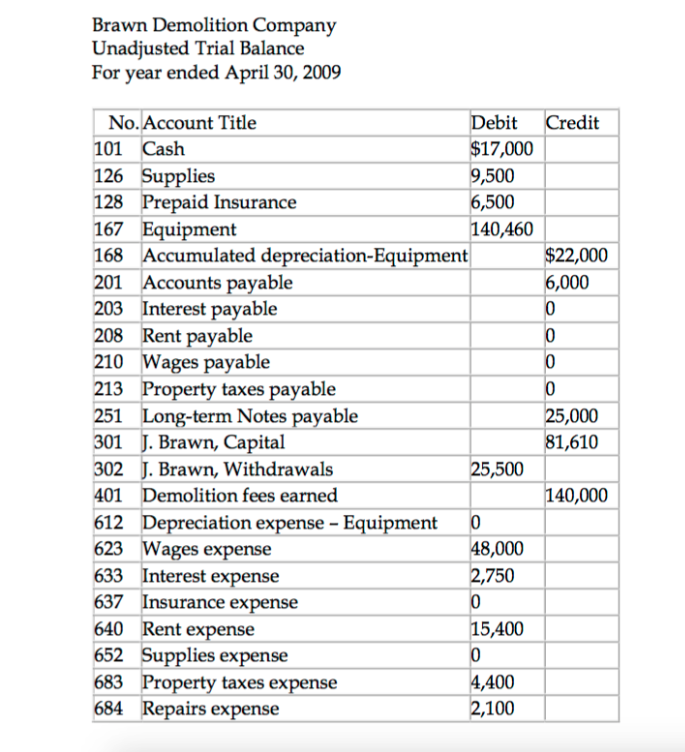

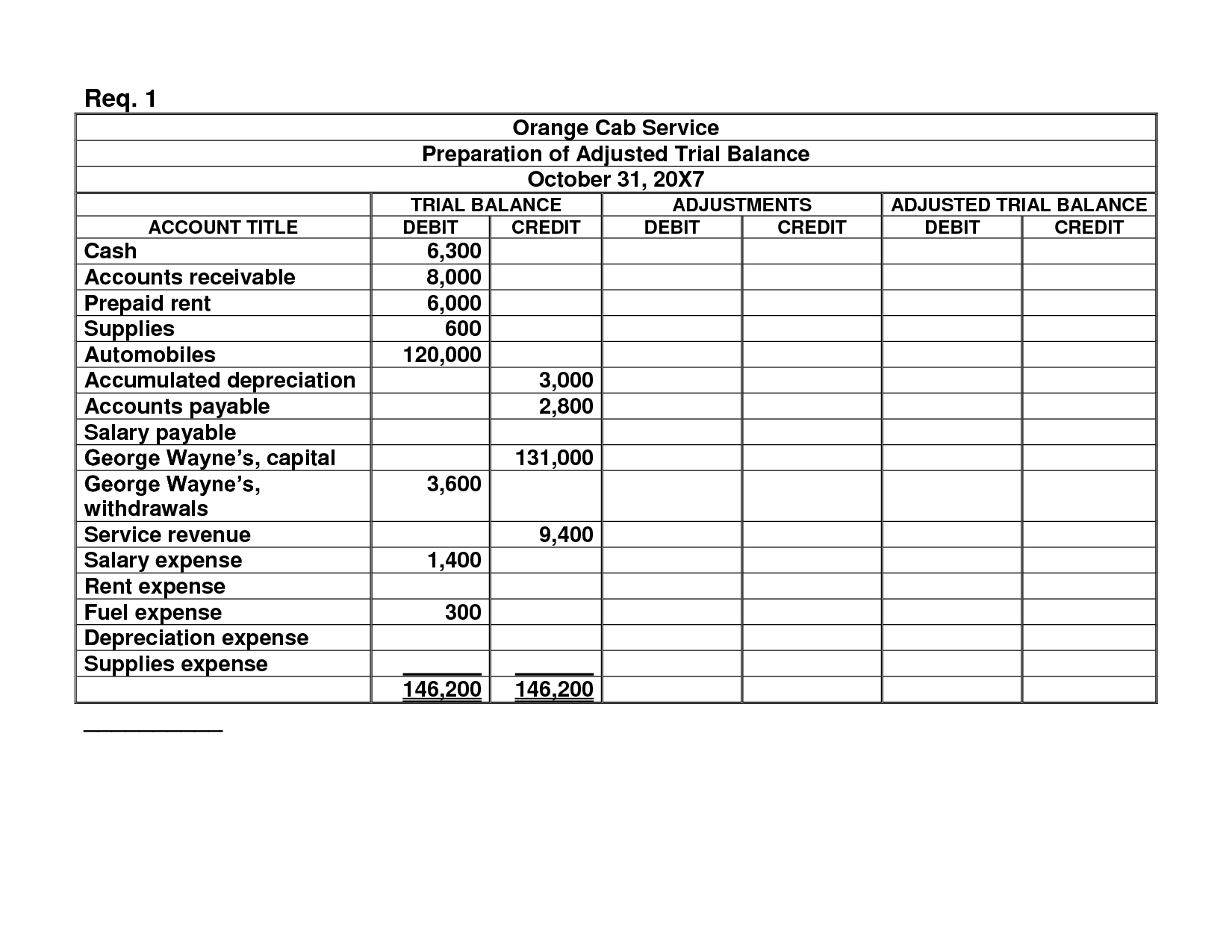

- Once all of the adjusting entries have been posted to the general ledger, we are ready to start working on preparing the adjusted trial balance.

The adjustments total of $2,415 balances in the debit and creditcolumns. After the adjusted trial balance is complete, we next preparethe company’s financial statements. An adjusted trial balance is prepared using the same format as that of an unadjusted trial balance. After the adjusted trial balance is complete, we next prepare the company’s financial statements. There were no Depreciation Expense and Accumulated Depreciation in the unadjusted trial balance. Because of the adjusting entry, they will now have a balance of $720 in the adjusted trial balance.

The accounting equation is balanced, as shown on the balance sheet, because total assets equal $29,965 as do the total liabilities and stockholders’ equity. Remember that the balance sheet represents the accounting equation, where assets equal liabilities plus stockholders’ equity. This is the second trial balance prepared in the accounting cycle.

However, it is the source document if you are manually compiling financial statements. In the latter case, the adjusted trial balance is critically important – financial statements cannot be constructed without it. Business owners and accounting teams rely on the trial balance to create reliable financial statements. A trial balance ensures the accuracy of your accounting system and is just one of the many steps in the accounting cycle. It’s one of the first lines of defense against accounting errors and a pivotal report within double-entry bookkeeping.

Looking at the income statement columns, we see that all revenue and expense accounts are listed in either the debit or credit column. This is a reminder that the income statement itself does not organize information into debits and credits, but we do use this presentation on a 10-column worksheet. Adjusted trial balance is not a part of financial statements; rather, it is a statement or source document for internal use. It is mostly helpful in situations where financial statements are manually prepared. If the organization is using some kind of accounting software, the bookkeeper or accountant just needs to pass the journal entries (including adjusting entries). The software automatically adjusts and updates the relevant ledger accounts and generates financial statements for the use of various stakeholders.

This means the $600 debit issubtracted from the $4,000 credit to get a credit balance of $3,400that is translated to the adjusted trial balance column. The statement of retained earnings (which is often a componentof the statement of stockholders’ equity) shows how the equity (orvalue) of the organization has changed over a period of time. Thestatement of retained earnings is prepared second to determine theending retained earnings balance for the period.

If the final balance in the ledger account (T-account) is a credit balance, you will record the total in the right column. The adjusted trial balance is the key point to ensure all debitsand credits are in the general ledger accounts balance beforeinformation is transferred to financial statements. Budgeting foremployee salaries, revenue expectations, sales prices, expensereductions, and long-term growth strategies are all impacted bywhat is provided on the financial statements.

These credit balances would transfer to the credit column on the adjusted trial balance. Adjusted Trial Balance refers to the general ledger balances reflecting adjustments, which include accrued expenditure and non-cash expenses. The list and the balances of the company’s accounts are presented after the adjusting journal entries are made at the year-end.